As we enter the current tax season, there are practical and timely considerations that may still influence your 2025 tax filing and help position you for success moving forward. Below are five areas worth reviewing, and a few changes to keep in mind as you plan for 2026 and beyond.

1. Make Last-Minute Retirement Contributions

You may still be able to contribute to an IRA for the 2025 tax year up until the filing deadline in April.

- Traditional IRA contributions may reduce your taxable income if you qualify.

- Roth IRA contributions do not reduce current taxes but can provide tax-free growth and withdrawals in retirement.

2025 IRA limits

- $7,000 contribution limit

- $1,000 additional catch-up if age 50+

Important note:

If you make a contribution before the filing deadline, tell your custodian the contribution is for the 2025 tax year so it is applied correctly.

2. Don’t Forget About Health Savings Accounts (HSAs)

If you are eligible for an HSA, you may still be able to contribute for 2025 before filing your return.

HSAs are often called one of the most tax-efficient savings tools because they offer:

- Tax-deductible contributions

- Tax-free investment growth

- Tax-free withdrawals for qualified medical expenses

Like IRA contributions, make sure you designate the correct tax year when contributing before the filing deadline.

3. Review Retirement Contribution Limits for 2026

While you’re filing your 2025 return, it’s also a good time to adjust your savings strategy for the new year.

Source: Captrust

The above chart shows the IRS-adjusted contribution limits for employer-sponsored retirement plans and IRAs over the past several years, along with the updated limits for 2026. Contribution limits for accounts like 401(k)s, 403(b)s, and IRAs are periodically increased to account for inflation and to encourage retirement savings. For example, the employee deferral limit for workplace retirement plans rises from $23,500 in 2025 to $24,500 in 2026, while catch-up contributions for individuals age 50 and older increase from $7,500 to $8,000.

401(k) Contribution Limits

Year Employee Contribution Limit

2025 $23,500

2026 $24,500

Additional contributions:

- Age 50+ catch-up

- 2025: $7,500

- 2026: $8,000

- Age 60–63 “super catch-up”

- Up to $11,250

New rule beginning in 2026

Under SECURE 2.0, certain higher-income employees (earning more than about $145,000 from the same employer) must make catch-up contributions on a Roth basis, meaning those contributions will no longer reduce current taxable income.

4. Revisit Your Deduction Strategy

Recent legislation introduced several deductions and changes that could affect how you approach your return.

Expanded SALT deduction

The deduction limit for state and local taxes (SALT) increased from:

- $10,000 → $40,000 beginning in 2025

For some taxpayers, particularly those in higher-tax states, this change may make itemizing deductions more beneficial than taking the standard deduction.

Source: Bipartisan Policy Center

The above graph illustrates how the expanded state and local tax (SALT) deduction cap applies across different income levels under the recent tax legislation. Beginning in the 2025 tax year, the maximum SALT deduction increases from $10,000 to $40,000 for taxpayers with adjusted gross income up to roughly $500,000. However, the benefit gradually phases out for higher-income households, declining at a set rate until the deduction returns to the prior $10,000 cap at income levels around $600,000.

New Temporary Deductions (2025–2028)

Additional deductions may include:

- Up to $6,000 senior deduction for taxpayers age 65+

- A deduction for interest on certain auto loans on qualified vehicles

- Deductions tied to certain tip income or overtime pay

Many of these deductions are temporary and income-dependent, so reviewing eligibility each year is important.

5. Plan Ahead for Changes in 2026

Several tax rules will begin changing in 2026, which may influence planning decisions today.

Charitable deduction changes

Beginning in 2026:

- Itemized charitable deductions must exceed 0.5% of AGI before becoming deductible.

- Non-itemizers may deduct up to:

- $1,000 (single)

- $2,000 (married filing jointly)

Estate and gift tax exemption

The federal exemption increases to:

- $15 million per individual starting in 2026

- Indexed for inflation going forward

This may create additional estate planning opportunities for high-net-worth families.

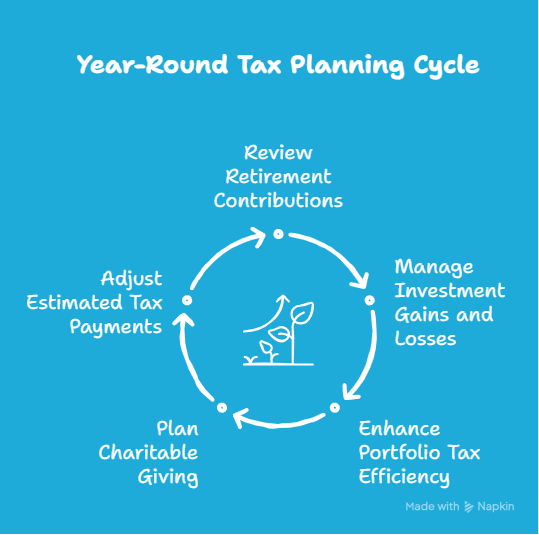

The Bigger Picture: Tax Planning Is Year-Round

Many of the most effective tax strategies happen before year-end, not just during filing season.

Areas worth reviewing throughout the year include:

- Retirement contributions

- Investment gains and losses

- Portfolio Tax Efficiency

- Charitable giving

- Estimated tax payments and withholdings

Source: Napkin AI

The above graphic highlights the idea that approaching tax planning as a continuous cycle rather than a once-a-year event may help identify opportunities to reduce taxable income, capture deductions, and improve overall tax efficiency over time.

Key Takeaways for This Tax Season

- There are still meaningful actions you can take before the mid-April deadline; that may influence your 2025 tax return.

- Recent tax law adjustments have reshaped thresholds, deductions, and credits, making it important to revisit planning fundamentals each year.

- Tax planning works best when integrated into your broader financial strategy, supporting goals like retirement readiness, legacy planning, and long-term wealth management.

Get in Touch

If you have questions about your tax situation or want to explore how tax planning fits into your broader financial plan and portfolio, we would love to help. Please reach out to Team Lake Oswego at [email protected] for a conversation or to schedule a review.