Frequently Asked Questions about Medicare and Enrollment Answered

If you’re age 65 and you’ve already enrolled in Medicare, or if you’ve helped a parent or someone else enroll in Medicare, you have most likely come to two conclusions:

- One: No one should receive that much mail; and

- Two: Enrolling in Medicare can be extremely confusing.

I agree with both.

The way that Medicare is delivered is perplexing, which can cause people to make the wrong decision when determining what coverage is best for them. Let’s unpack a few of the most commonly misunderstood aspects of Medicare.

Do I Have to Enroll in Medicare at Age 65?

The short answer is: not always.

If you are still working (or if your spouse is still working and you are covered under his or her plan with creditable coverage), you don’t have to enroll in Medicare.

Creditable coverage is defined as health insurance, prescription drug or other health benefit plans that meet a minimum set of qualifications. If you aren’t sure that your coverage is credible, contact your HR team for clarification.

It’s important to note that COBRA coverage, in which you stay on your old employer’s health plan after a job loss or other qualifying event, is not creditable insurance.

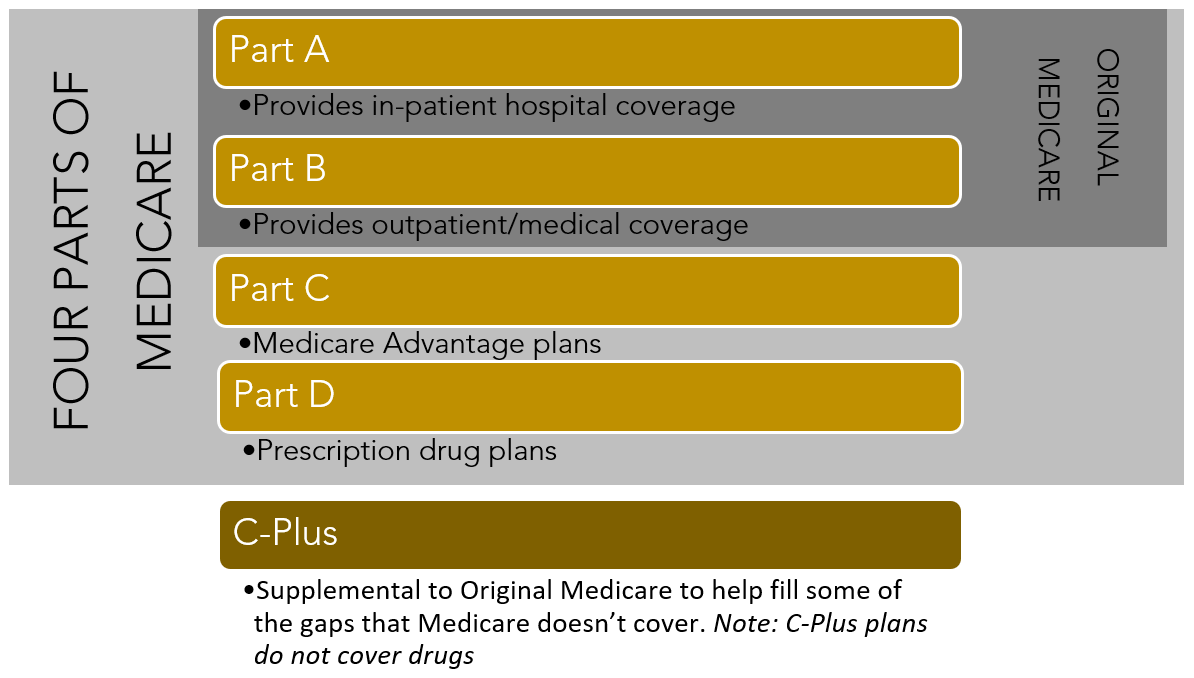

What Are the Different Parts of Medicare?

There are four main parts of Medicare: Parts A, B, C and D. Each has a specific purpose as outlined below.

- Part A: Provides in-patient hospitalization

- Part B: Provides outpatient/medical coverage

- Part C: Medicare Advantage plans

- Part D: Prescription drug plans

- C-Plus: Supplemental to Original Medicare to help fill some of the gaps that Medicare doesn’t cover. Note: C-Plus plans do not cover drugs

What Are My Medicare Options: Original Medicare vs. Medicare Advantage Plans?

When enrolling in Medicare, there are two main options: Original Medicare and Medicare Advantage.

Original Medicare is a fee-for-service program where beneficiaries can obtain care from any participating provider. Original Medicare is 80%/20% coverage, meaning the insurance company pays 80% of costs and the insured is responsible for the remaining 20%.

Original Medicare includes Part A (hospitals) and Part B (doctors, outpatient and medical equipment) coverage. Medicare does not cover prescription drugs so people enrolled in Original Medicare will also need to purchase a stand-alone Part D (prescription drug) plan.

If you have Original Medicare, you have the option to purchase a C-Plus (also known as Medigap) policy. A C-Plus policy helps cover the gaps (the 20% you are financially responsible for) that Medicare doesn’t cover. If you travel a lot, have kids out-of-state that you visit often or want to purchase a Medigap (or C-Plus) policy, Original Medicare may be the right plan for you.

Medicare Advantage (also known as Part C) plans are an alternative way to receive benefits under Medicare. These plans are sold by private insurers. If you have a Medicare Advantage plan, you still have Medicare and will still owe a monthly Part B premium.

Each Medicare Advantage Plan must provide all Part A and Part B services covered by Original Medicare, but can do so with different rules, costs and restrictions that can affect how and when you receive care. Medicare Advantage Plans can also provide Part D coverage.

It’s important to understand your Medicare coverage choices and to choose your coverage carefully. How you choose to get your benefits and who you get them from can affect both your out-of-pocket costs and where you can get your care.

For example, in Original Medicare you are covered to go to nearly all doctors and hospitals in the country as long as they take Medicare patients. However, Medicare Advantage Plans usually have network restrictions, meaning that you will be more limited in your access to doctors and hospitals. Medicare Advantage Plans may still be the best option for you as they can also provide additional benefits that Original Medicare does not cover, such as routine vision or dental care.

What About Part D Prescription Drug Plans?

Medicare drug plans cover generic and brand-name drugs. All plans must meet a standard level of coverage set by Medicare. This means they must all cover the same categories of drugs, but plans can choose which specific drugs are covered in each drug category.

Plans can change from year to year, new plans become available, and the drugs that you are taking can change, so one of the most important things to do is stay up to date on your prescription drug plan. Each year during Medicare open enrollment (October 15th – December 7th), you can change your drug plan. Your pharmacist will be able to evaluate the best plan for you based on the drugs that you are currently taking.

Copays, tiered pricing and various restrictions can cause the price of drugs to vary from plan to plan. It’s important to research your coverage options thoroughly to find the plan that best fits your needs.

Where Can I Get More Answers to My Questions About Signing Up for Medicare?

Medicare is a complicated healthcare system, and finding the right plan depends on many factors, like your prescriptions, physician preferences and finances.

Waverly Advisors can help you make sense of it all. If you’re getting ready to sign up for Medicare and have questions, ask an advisor to reach out to you to start the conversation and walk through your options with you.

Disclosure: You should not assume that any information provided serves as the receipt of, or as a substitute for, personalized investment advice from Waverly Advisors. This information should be used as a reference only. Talk to your Waverly Advisors, or a professional advisor of your choosing, for guidance specific to your situation.