Risk of Concentration

“Don’t risk what you have and need to pursue what you don’t have and don’t need.” – Warren Buffett on investment risk

When asked about the merits of diversification Warren Buffett quipped, “it makes little sense if you know what you’re doing.”

Hedge fund ace Stanley Drunkenmiller was asked a similar question about diversification, “I like putting all my eggs in one basket and then watching that basket very closely.”

On financial social media (X.com), you’ll find amateur investors blindly following their investment heroes.

Here’s the thing; an investor needs to understand and define the game they are playing.

Most investors arguing, debating, or touting their own investment approach are people playing different games.

The young ambitious entrepreneur quits her job to start her own company.

The mid-20’s technology employee receives the bulk of her compensation in stock options.

The newly retired engineer needs $80,000 per year from their investment portfolio.

These people are allocating capital to financial markets, but playing radically different games.

For a young, early/mid-career person, concentration makes sense.

- Large runway to recover if things go poorly

- For most early career folks, their balance sheet is much smaller (if wiped out there’s less dollars at stake).

- If they do strike gold, they have their entire life to enjoy the payoff

- Failing early in one’s career can be extremely valuable (assuming they learn from the lesson)

For someone retired or about to retire, concentration risk can be perilous. Even worse if the concentration bet is made unknowingly.

- Unable to recover if things go poorly, which increases the risk of running out of money, going back to work, downsizing lifestyle, etc.

- For retirees, there’s usually bigger dollar amounts at stake

- If they do strike gold, the larger portfolio isn’t likely to change their lifestyle (however, tanking their portfolio would adversely affect their financial plan).

- Failing to manage financial affairs towards the end of your journey would maximize the pain of regret

In our opinion, taking large, concentrated bets for a retiree is a dangerous game. A good rule of thumb is to avoid risks where the best-case outcome won’t change your life, but the worst case would devastate your retirement dreams.

Concentration risk within a retirement portfolio can show up in several ways. Here are the most common large, active bets we see in prospective client portfolios…

Magnificent 7 (direct ownership)

It wouldn’t be a stretch to say 9/10 prospective client portfolios have an overallocation to big technology companies. This has been a great place to be; with outsized gains, soaring revenues, and the leaders of the AI revolution.

However, this is a massive bet on a momentum technology index. Worse yet, most people are blind to their total exposure or potential drawdowns.

No one notices concentration risk on the way up. Most aren’t ready for the other side of concentration risk on the way down (which usually occurs much quicker).

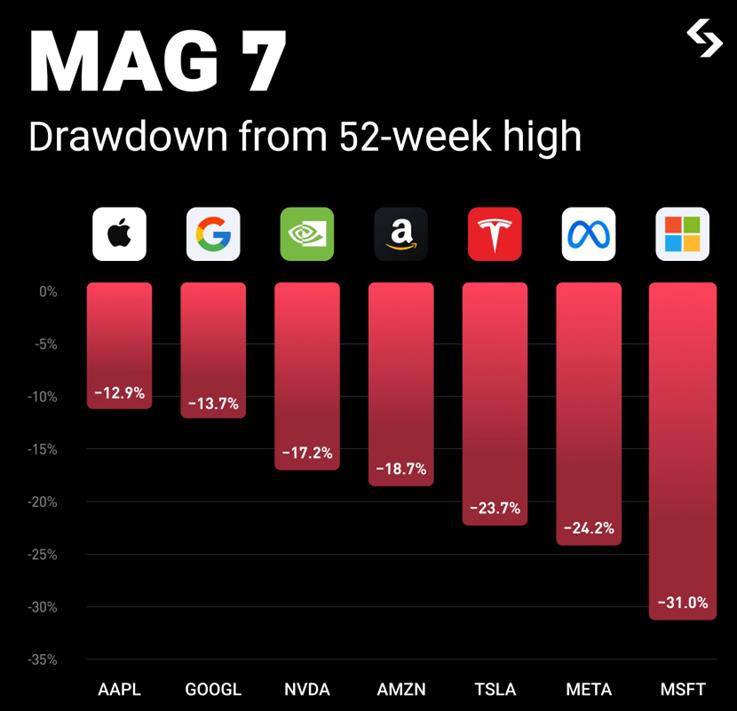

Source: Bitget, X.com

The above chart is a snapshot of the Mag 7 stocks drawdown from their 52-week high (March 2026). A trade is crowded when everyone owns it, the holdings dominate benchmarks (i.e. S&P 500), and sentiment is overwhelmingly positive. The Mag 7 check all three boxes.

U.S. Households are All-In Stocks

U.S. household ownership equities is a great historical data point for future returns.

When stock ownership is high, future returns tend to be lower.

When stock ownership is low, future returns tend to be higher.

As of the end of 2025, U.S. household ownership of stocks is at an all-time high…

Source: Board of Governors of the Federal Reserve

The above chart shows the percentage of stocks that U.S. households and non-profits own. Notice how cycle peaks are consistent with market selloffs. Recent examples include the technology bubble (1999), COVID (2020), and 2021.

Home Country Bias

Not only are U.S. investors allocating more of their resources to stocks, but there’s also a strong home country bias. Investors tend to over-allocate to their home market because of perceived lower risk, recent outperformance, lower transaction costs, and familiarity with U.S.-based companies.

Despite U.S. markets making up ~50-55% of global equities, it’s estimated that U.S investors own 70-80% of domestic companies. That’s a large, active bet on U.S. stocks.

In our opinion, retirees would do well to examine the investment universe beyond the S&P 500, technology sector, and Mag 7 stocks.

——————————————————————————————————————

We aren’t sounding the alarm for an imminent blow up in U.S. stocks. However, an investor should clearly identify the game they are playing.

For a young, early/mid-career person, concentration makes sense.

For someone retired or about to retire, concentration risk can be perilous (especially if you’re unknowingly making a concentrated bet).

Nobel laureate Harry Markowitz famously said, “Diversification is the only free lunch in investing.”

If you want to understand how to build a tax-efficient, diversified retirement portfolio, shoot us a note at [email protected].

Written by Nik Schuurmans, CFA®

Nik Schuurmans joined Waverly Advisors in January 2026 after Pure Portfolios was acquired by Waverly Advisors, LLC. As Partner and Wealth Advisor, Nik operates using a transparent and pioneering fee structure, to provide a modern wealth management experience for every client. Nik believes access to professional advice should not come with exorbitant fees, misaligned incentives, and conflicts of interest. Learn more about Nik…

Important Disclosure Information – Waverly Advisors (waverly-advisors.com)

Disclosure: Past performance may not be indicative of future results. The opinions expressed in this commentary reflect information available at the time it was written and should be used as a reference only. Due to various factors, including changing market conditions, economic conditions, and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Waverly. If you have any questions regarding the applicability of any specific issue discussed above to your individual situation, you are encouraged to consult with your Waverly adviser or the professional advisor of your choosing. A copy of Waverly’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or by visiting https://waverly-advisors.com/ADV-Part-2A-Brochure. Please see additional important disclosures on the last page of this report.