Mid-Year Check In – Are Your 2026 Financial Goals on Track?

We’re halfway through 2026 — summer is in full swing, vacations are on the calendar, and December feels far away. Mid-year is a great time for a quick check-in on your financial goals. There’s still time to course-correct, and the decisions are smaller than the ones you might be making in a hurry in December.

Here’s what’s worth a look as we head into the second half of the year.

1. Savings Goals – Are You on Pace?

Whether your 2026 goal was building an emergency fund, paying down debt, saving for something specific, or maxing out retirement contributions — now is the time to check in on your progress.

Start by confirming which limits apply to you and where your year-to-date contributions stand.

2026 Retirement Contribution Limits

- 401(k), 403(b), 457 and TSP plans: The employee deferral limit is $24,500 for 2026. If you’re 50 or older, you can add another $8,000. If you’re between 60 and 63, your “super catch-up” jumps to $11,250.

- IRAs: $7,500 for 2026, with an additional $1,100 catch-up at 50 and older.

529 Contributions

- If you’re funding a 529, check the balance and year-to-date contributions now. Many states offer a tax deduction or credit for contributions.

Taxable Account Savings

- A taxable brokerage account offers flexibility for short to mid-range goals — the down payment, the next car, a home renovation, a wedding. In addition, saving in this bucket ensures you have multiple tax options for retirement spending.

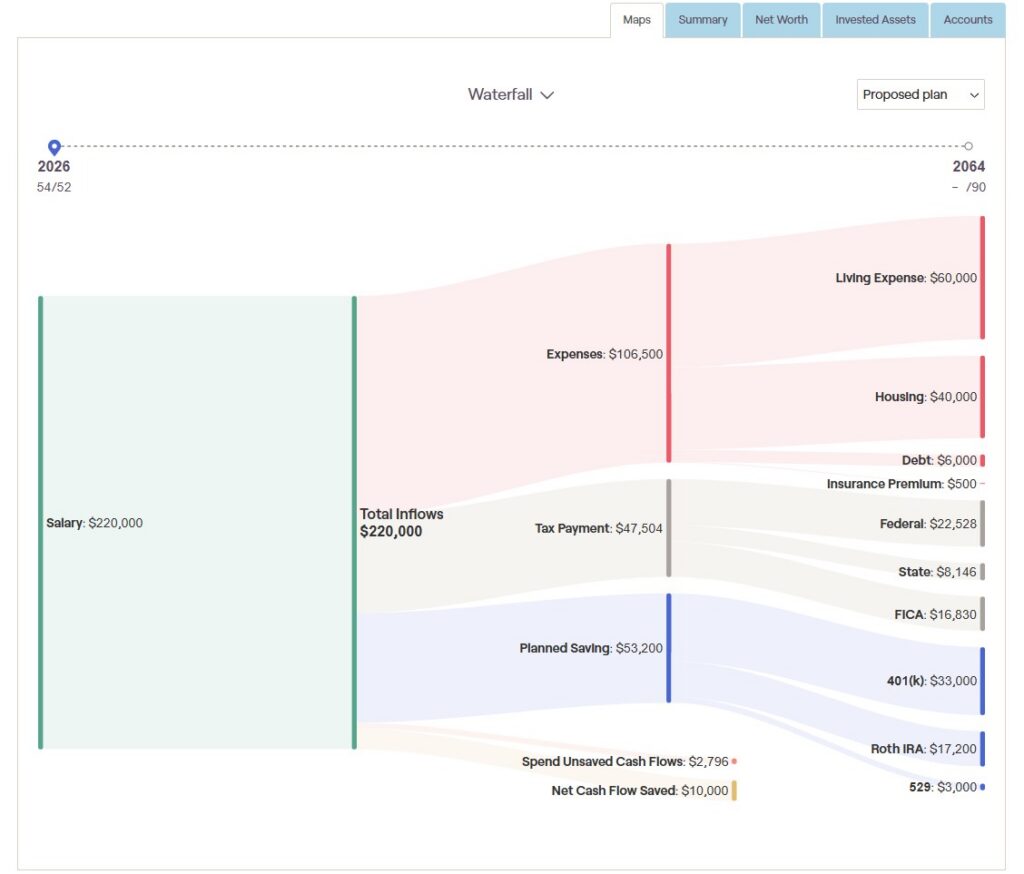

The chart below comes from a sample client’s financial plan, showing where their dollars are projected to flow this year — living expenses, taxes, savings, and planned goals. Looking at the year this way often surfaces small mismatches between what was intended and what’s actually happening.

Source: RightCapital (7/1/2026)

The chart shows how projected income flows through the year — taxes, living expenses, debt payments, savings, goals. Mid-year is often when you can see whether you are on track with your planned goals, if you’ll have a cash surplus, or if you’re falling short.

2. Revisit Your Tax Picture for 2026

The best tax planning happens throughout the year, not just at filing time. By July, you have enough of the year behind you to estimate your income for the year, and enough ahead of you to actually do something about it.

A few things worth reviewing now:

- Capital Gains and Tax Loss Harvesting

Review the unrealized gains and losses in your taxable accounts. If you have realized gains already, they may create a tax bill next April unless you plan ahead. Tax-loss harvesting — selling investments at a loss to offset gains — can help manage that impact, but the bigger goal is to understand where you stand now and set expectations for any potential tax liability before year-end.

- New Deductions to Check

The One Big Beautiful Bill Act added several new deductions for 2025–2028 — an additional senior deduction, plus provisions for auto loan interest, tips, and overtime income. Most have income limitations, so it’s worth confirming eligibility before counting on them.

- Roth Conversion Opportunities

If 2026 is shaping up as a lower-income year —in between jobs, recently retired, or in a gap before Social Security starts — that’s a window worth using. A partial Roth conversion lets you move money from a Traditional IRA into a Roth at today’s rates, locking in tax-free growth for the rest of your life. The same logic applies if you see RMDs pushing you into a higher bracket down the road.

Here’s an example of how a multi-year Roth conversion strategy might be modeled before RMDs begin — using the lower-income years to deliberately fill up the bracket you’re already in.

Source: RightCapital(7/1/2026)

A sample Roth conversion analysis. The idea is to pay some tax voluntarily today — at a rate you can see and choose — in exchange for tax-free withdrawals later. The right amount depends on your income, marginal bracket, time horizon, and legacy goals, so the analysis is always specific to each client.

3. RMDs: Don’t Wait Until December

If you’re subject to Required Minimum Distributions (RMDs) from an IRA or inherited IRA, get the plan in place now.

- Confirm the 2026 RMD amount has been calculated.

- Decide whether to take it as one distribution or spread it across the year — spreading often makes cash flow planning easier.

- Consider a Qualified Charitable Distribution if you’re charitably inclined and over 70.5 years old. A QCD sends part (or all) of your RMD directly to a qualified charity, satisfies the distribution requirement, and keeps the amount out of your taxable income entirely.

4. Annual Gifting

Most people leave gifting until December. Handling it now takes one item off the year-end list.

- Gifting to Individuals: The annual federal gift exclusion is $19,000 per recipient in 2026 — $38,000 if you and your spouse split the gift — with no gift-tax return required.

- Charitable Giving: Beginning in 2026: itemized charitable deductions must exceed 0.5% of your AGI before any of the gift becomes deductible. Non-itemizers get something they didn’t have before — an above-the-line deduction of up to $1,000 single or $2,000 married filing jointly. Both changes are worth a closer look before deciding how and when to give this year.

Your Mid-Year Financial Checklist

A quick reference for what to confirm before heading into the fall.

| Review Items | Status |

| Savings contributions on pace for 2026 | Yes | No |

| Roth conversion opportunity identified (if applicable) | Yes | No | N/A |

| RMD taken (if applicable) | Yes | No | N/A |

| Tax withholding / estimated payments on track | Yes | No |

| Emergency fund intact | Yes | No |

| Beneficiary designations reviewed | Yes | No |

| Insurance coverage reviewed | Yes | No |

| Year-end gifting strategy started | Yes | No | Not yet |

Get in Touch

Whether it’s savings, a Roth conversion, charitable giving, or simply a second set of eyes on the plan, we’re glad to help. Reach out to Team Lake Oswego at [email protected] to start a conversation, or your Advisor to schedule a review.

Interested in creating your own financial plan? Reach out to our team or click here to get started.

Written by Tim Metz

Written by Tim Metz

Tim Metz joined Waverly Advisors in January 2026 after Pure Portfolios was acquired by Waverly Advisors, LLC. As a Wealth Advisor at Waverly, Tim brings years of experience in Investment Management, Retirement Planning, Family Office, and Trust Companies. Tim is passionate about solving complex financial issues and partnering with clients to understand them. Learn More About Tim…

Written by Sami Gianella, CPA

Written by Sami Gianella, CPA

Sami Gianella joined Waverly Advisors in February 2026 following the acquisition of Pure Portfolios by Waverly Advisors, LLC. As an Associate Wealth Advisor at Waverly, Sami brings experience in investment management, comprehensive financial planning, estate review, tax strategy, and charitable and family gifting. Sami is passionate about helping clients develop their financial goals and partnering with them to build thoughtful, personalized strategies to achieve them. Learn More About Sami…

IMPORTANT DISCLOSURES

THE INFORMATION PRESENTED IN THIS DOCUMENT IS FOR GENERAL INFORMATIONAL AND EDUCATIONAL PURPOSES, AND IS NOT SPECIFIC TO ANY INDIVIDUAL’S PERSONAL CIRCUMSTANCES. NOTHING IN THIS DOCUMENT CONSTITUTES, OR SHALL BE RELIED UPON AS INVESTMENT, LEGAL, OR TAX ADVICE TO ANY PERSON. THE INFORMATION IN THIS DOCUMENT IS PROVIDED EFFECTIVE AS OF THE DATE OF ITS PUBLICATION, DOES NOT NECESSARILY REFLECT THE MOST CURRENT STATUS OR DEVELOPMENT, AND IS SUBJECT TO REVISION AT ANY TIME. INVESTING INVOLVES RISK, AND PAST PERFORMANCE DOES NOT NECESSARILY PREDICT FUTURE RESULTS. NONE OF WAVERLY, OR ANY OF ITS OFFICERS, MEMBERS OR AFFILIATES, IN ANY WAY WARRANT OR GUARANTEE THE SUCCESS OF ANY ACTION THAT ANYONE MAY TAKE IN RELIANCE ON ANY STATEMENTS OR RECOMMENDATIONS IN THIS DOCUMENT.

WAVERLY ADVISORS, LLC (“WAVERLY”) IS AN SEC-REGISTERED INVESTMENT ADVISER. A COPY OF WAVERLY’S CURRENT WRITTEN DISCLOSURE BROCHURE AND FORM CRS (CUSTOMER RELATIONSHIP SUMMARY) DISCUSSING OUR ADVISORY SERVICES AND FEES REMAINS AVAILABLE AT HTTPS://WAVERLY-ADVISORS.COM/. YOU SHOULD NOT ASSUME THAT ANY INFORMATION PROVIDED SERVES AS THE RECEIPT OF, OR AS A SUBSTITUTE FOR, PERSONALIZED INVESTMENT ADVICE FROM WAVERLY ADVISORS, LLC (“WAVERLY”). THIS INFORMATION SHOULD BE USED AS A REFERENCE ONLY. TALK TO YOUR WAVERLY ADVISOR, OR A PROFESSIONAL ADVISOR OF YOUR CHOOSING, FOR GUIDANCE SPECIFIC TO YOUR SITUATION. PLEASE NOTE: THE SCOPE OF THE SERVICES TO BE PROVIDED DEPENDS UPON THE NEEDS OF THE CLIENT AND THE TERMS OF THE ENGAGEMENT.

INVESTMENT ADVISORY SERVICES ARE OFFERED BY WAVERLY ADVISORS, LLC, AN INVESTMENT ADVISER REGISTERED WITH THE SECURITIES AND EXCHANGE COMMISSION. © 2024 WAVERLY ADVISORS, LLC. ALL RIGHTS RESERVED.