Estate Planning in the Pacific Northwest: What You Should Know

Estate planning is often associated with federal estate taxes and ultra-high-net-worth households; however, for families in Oregon and Washington, state-level estate taxes can create planning considerations at much lower asset levels.

While the federal estate tax exemption has increased significantly, both Oregon and Washington impose estate taxes with much lower thresholds, making proactive planning especially important.

Federal Estate Tax: Less Relevant for Many Households

The One, Big, Beautiful Bill (OBBB) signed into law in 2025 increased the federal estate and gift tax exemption to $15 million per individual beginning in 2026, indexed for inflation.

- Many families will not be subject to federal estate tax

- Federal tax rates still reach up to 40% for larger estates

- Planning remains important for ultra-high-net-worth households

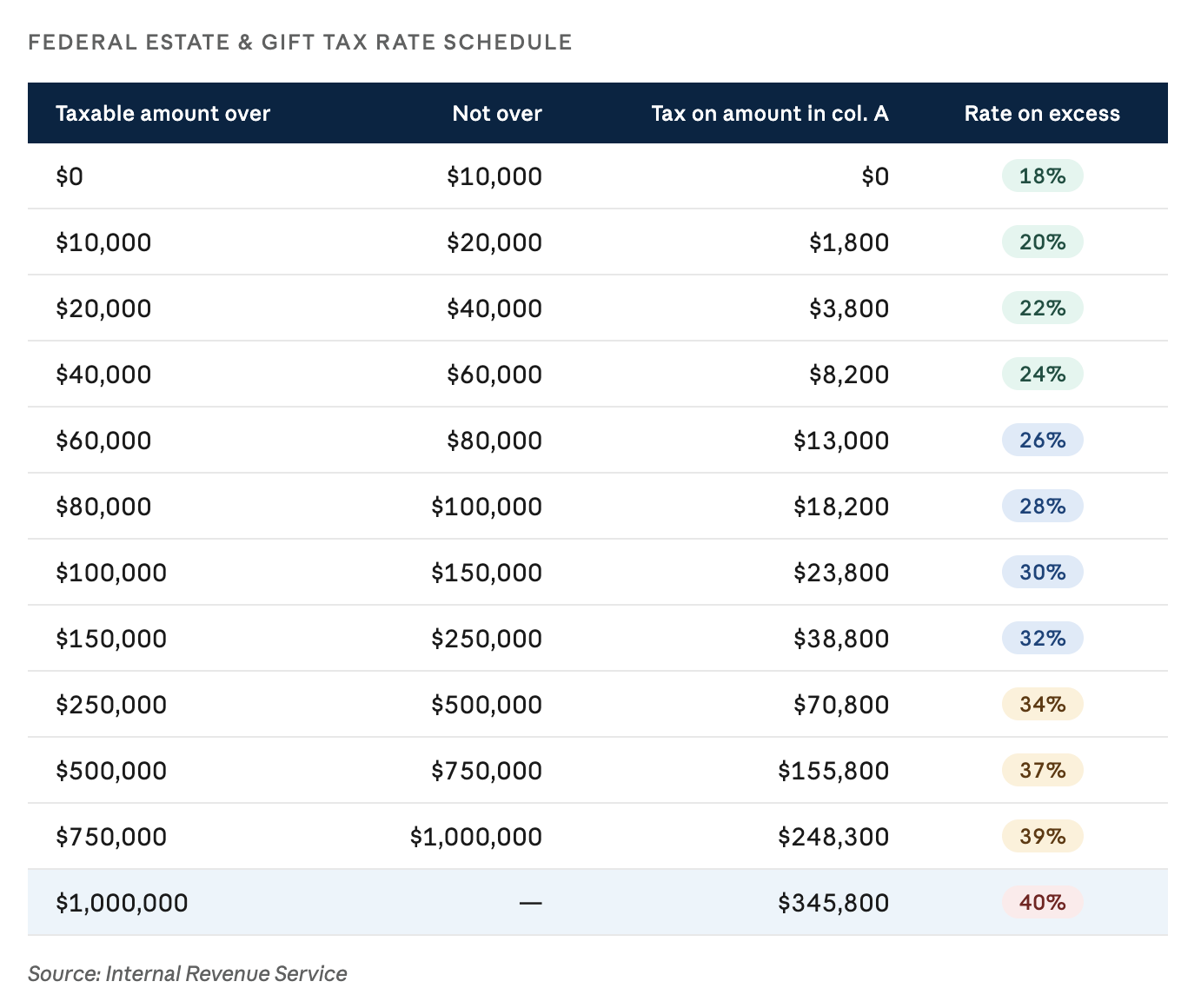

Source: Internal Revenue Service

The chart above outlines the federal estate tax rate schedule applied to taxable estates exceeding the exemption amount. It highlights the progressive structure of the system, where marginal tax rates increase as estate values rise.

Key takeaway:

For many Oregon and Washington residents, state estate taxes, not federal, may be the primary concern.

Oregon State Estate Tax: Low Threshold, Broad Impact

Oregon has one of the most restrictive estate tax systems in the country:

- $1,000,000 exemption per individual

- Not indexed for inflation

- Tax rates range from 10% to 16%

As a result, estates that would not be subject to federal estate tax may still face state-level taxation in Oregon. It is possible for legislation to increase the estate tax exemption in the future, but nothing has been passed to date.

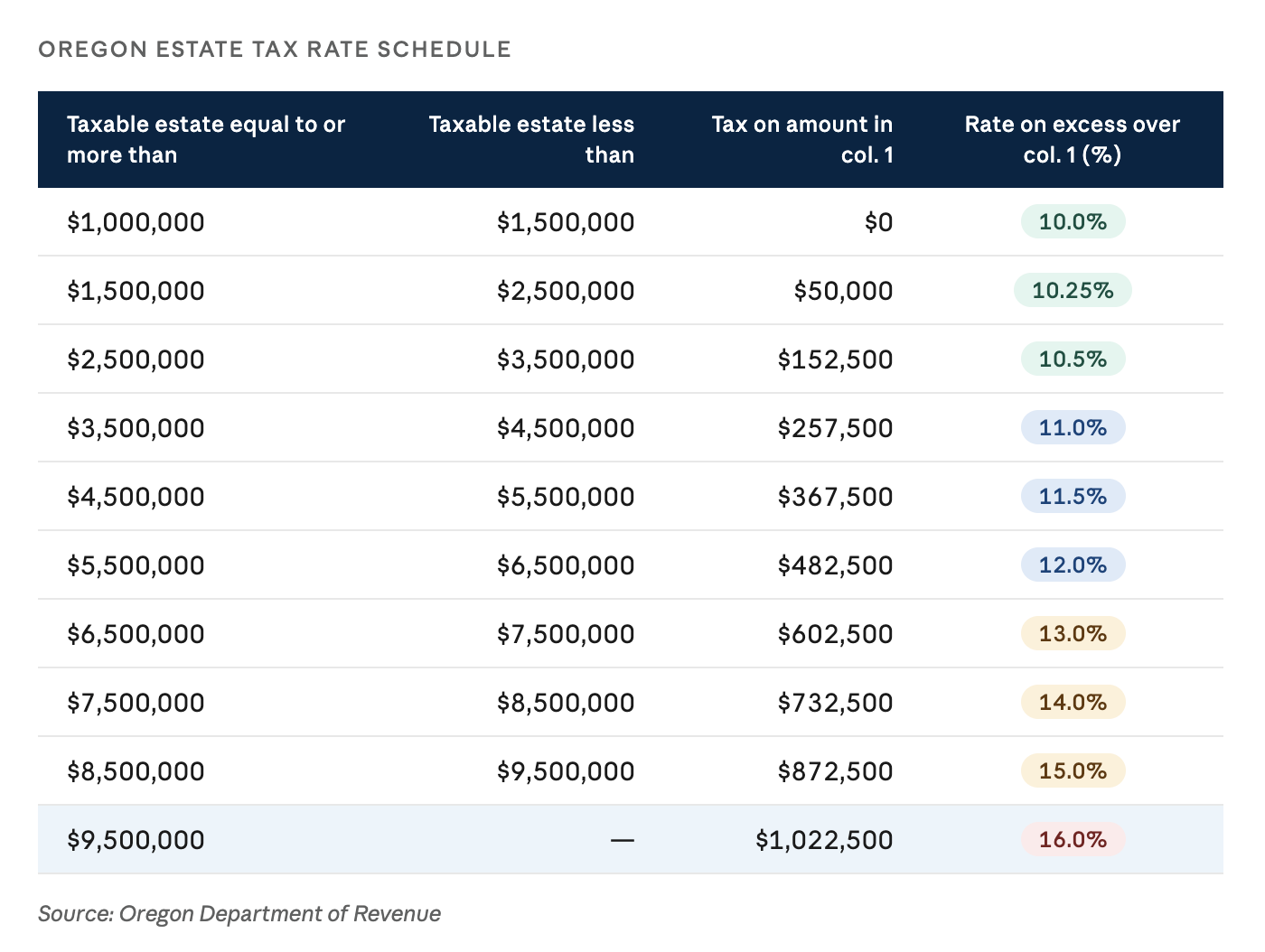

Source: Oregon Department of Revenue

The chart above summarizes Oregon’s estate tax structure, illustrating how taxes apply once the $1 million exemption threshold is exceeded. It reflects the state’s progressive rate system, with tax liability increasing incrementally as estate values grow.

Washington State Estate Tax: Higher Threshold, Higher Rates

Washington provides a higher exemption but imposes steeper tax rates:

- Approximate exemption of $3,076,000 per individual (inflation-adjusted)

- Tax rates range from 10% up to 35%

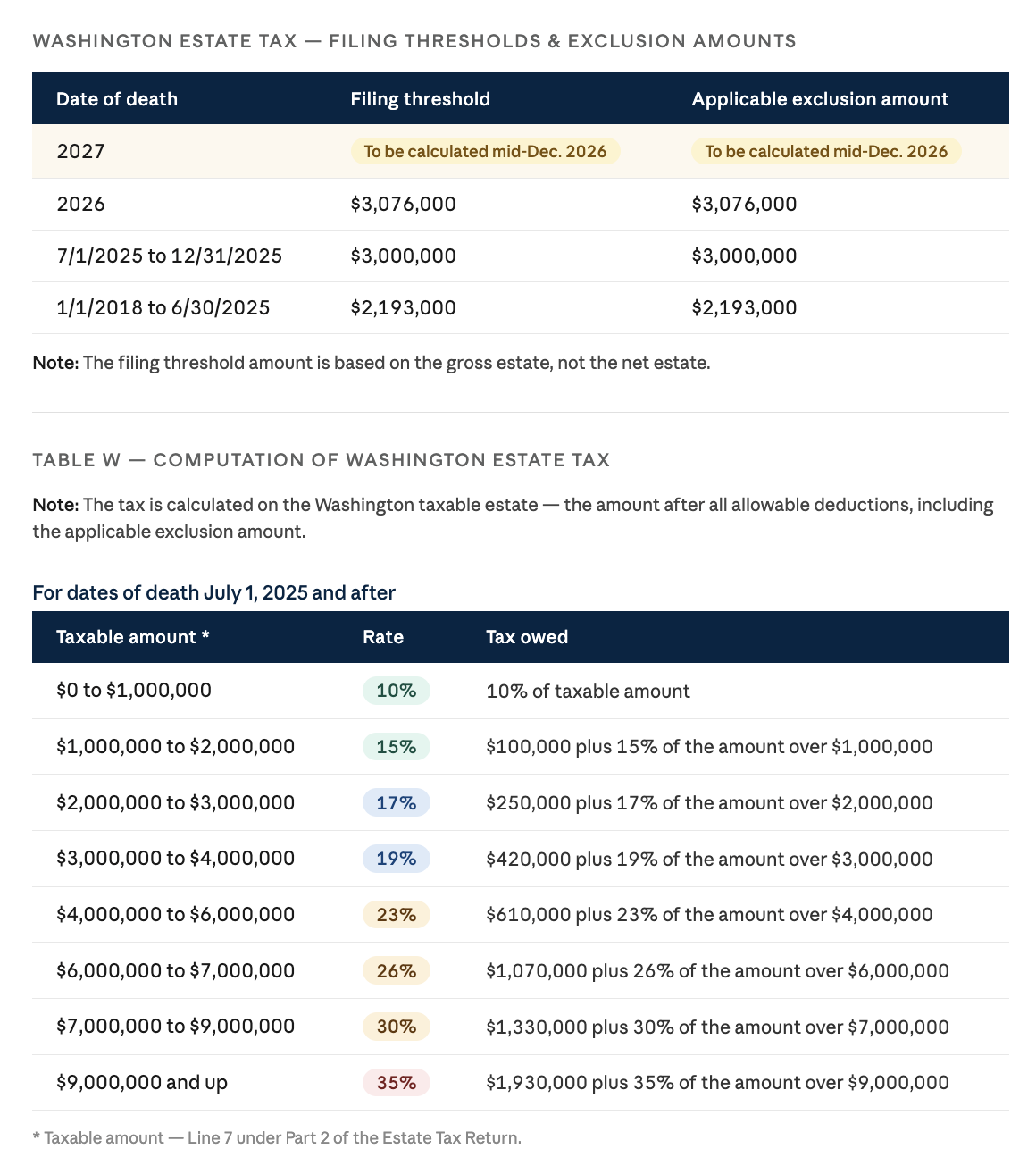

Source: Washington Department of Revenue

The charts above provide an overview of Washington’s estate tax framework. The top section illustrates changes to the state exemption amount over time, while the bottom table outlines the progressive tax rates applied to estates exceeding the exemption.

Key takeaway:

- Fewer households are impacted compared to Oregon

- However, those above the threshold may face significantly higher marginal tax rates

State Level Estate Tax Planning Strategies

For those with potential state estate tax exposure, several strategies may be worth evaluating:

1. Moving State of Residency

- Most states do not have an estate tax and relocating state of residency can avoid a state level tax (for example – Nevada, Arizona, and Idaho)

2. Lifetime Gifting

- Reduces taxable estate by transferring assets during life

- Annual federal gifting exclusion: $19,000 per recipient

- Larger gifts can be made utilizing part of the individual’s federal lifetime exemption

Considerations:

- No step-up in basis on gifted assets as there is with inherited assets which can make it more tax efficient to gift cash and high-basis assets

- Beneficiaries usually find higher utility for money earlier in life (in their 20s & 30s) rather than inheriting later when they’re more financially established

3. Charitable Giving:

- Direct donations to charity or setting up a Charitable Remainder Trust reduce the overall taxable estate

Planning insight:

- Leaving traditional IRA assets to charity can be a tax-efficient way to give as it preserves tax free assets and assets that receive a step-up-in-basis for heirs (taxable accounts, Roth accounts, and real estate)

4. Trust Strategies:

- Irrevocable trusts created during an individual’s lifetime remove assets from the taxable estate

- Irrevocable Life Insurance Trusts (ILITs) keep insurance death benefit proceeds outside of the taxable estate

5. Planning for Married Couples (Critical in OR/WA)

- No portability of state exemptions in Oregon or Washington to the surviving spouse

Key takeaway:

- Without proper planning, one spouse’s exemption may be lost if the first spouse to pass leaves everything to the surviving spouse

Common approach:

- Funding a Credit Shelter (Bypass) Trust at the first death utilizing that spouse’s full exemption ensures that everything is not left to the surviving spouse’s estate value with their single individual exemption

- This strategy is often built into revocable living trust documents in states that impose an estate tax

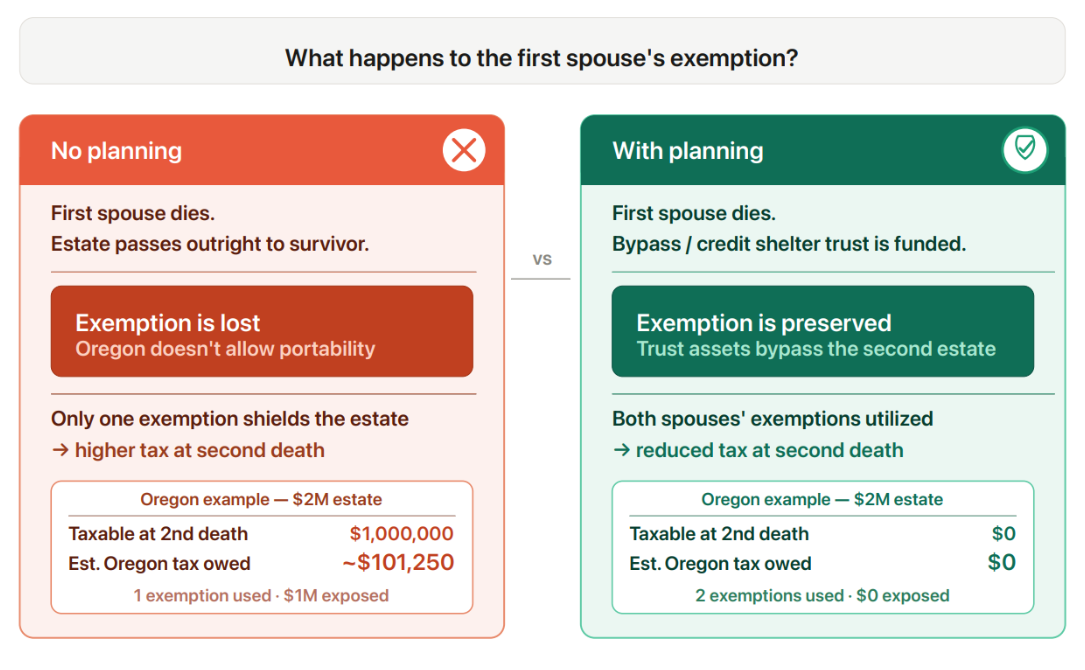

Sources: Oregon Department of Revenue; Internal Revenue Service

The graphic above illustrates how Oregon’s lack of state estate tax exemption portability affects married couples. When assets pass outright to a surviving spouse, the first spouse’s exemption may be lost, increasing potential estate tax exposure at the second death.

Bringing It All Together

For many families in Oregon and Washington, estate planning is less about federal thresholds and more about navigating state-specific rules.

- You may owe no federal estate tax

- But still face meaningful state-level tax exposure

A thoughtful plan incorporating gifting, trusts, and coordinated estate structures can help support efficient wealth transfer and alignment with your long-term goals.

Get in Touch

If you have questions about estate planning, we would love to help. Please reach out to Team Lake Oswego at [email protected] for a conversation or to schedule a review.

Written by Sami Gianella, CPA

Sami Gianella joined Waverly Advisors in February 2026 following the acquisition of Pure Portfolios by Waverly Advisors, LLC. As an Associate Wealth Advisor at Waverly, Sami brings experience in investment management, comprehensive financial planning, estate review, tax strategy, and charitable and family gifting. Sami is passionate about helping clients develop their financial goals and partnering with them to build thoughtful, personalized strategies to achieve them. Learn More About Sami…

Important Disclosure Information – Waverly Advisors (waverly-advisors.com)

Disclosure: Waverly Advisors, LLC (“Waverly”) is an SEC-registered investment adviser. A copy of Waverly’s current written disclosure Brochure and Form CRS (Customer Relationship Summary) discussing our advisory services and fees remains available at https://waverly-advisors.com/.Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Waverly Advisors, LLC, or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Forward-looking statements cannot be guaranteed. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any information provided serves as the receipt of, or as a substitute for, personalized investment advice from Waverly Advisors.”

Back to Resources