Understanding distribution rules, tax implications, and withdrawal strategies

For many retirees, building wealth is only part of the financial journey. Eventually, the focus shifts from accumulation to distribution, and that transition can introduce a new set of decisions. Required Minimum Distributions (RMDs), represent one of the most important and often misunderstood aspects of retirement planning.

RMDs are mandatory withdrawals from certain retirement accounts that begin once an individual reaches a specified age. These distributions apply to many tax-deferred retirement accounts, including traditional IRAs and employer-sponsored retirement plans such as 401(k)s. While the rules surrounding RMDs are designed to ensure retirement accounts are eventually taxed, they can also introduce complex planning considerations.

Without thoughtful preparation, RMDs may create unintended tax consequences, disrupt long-term investment strategies, or accelerate the depletion of retirement assets. For individuals and families managing significant retirement savings, the impact can be substantial.

However, when approached strategically, RMD planning may become an opportunity rather than simply a regulatory requirement. Decisions around timing, withdrawal strategies, tax planning, and coordination with other income sources can influence the sustainability of retirement income and the long-term preservation of wealth.

This guide explores the key considerations surrounding Required Minimum Distributions. It outlines how RMD rules work, the potential tax implications they may create, and the planning strategies individuals may consider as part of a broader retirement income framework.

Retirement Distribution Timeline

Understanding Required Minimum Distributions

Required Minimum Distributions exist for retirement accounts funded with pre-tax contributions. Pre-tax contributions defer taxation during the accumulation phase. To prevent perpetual deferral, Congress requires that these accounts begin distributing funds at specified ages with the goal of depleting the accounts (and earning the government receipt of the taxes) during a retirees lifetime.

Although the concept may appear straightforward, the rules governing RMDs have evolved over time and can vary depending on account type, ownership structure, and retirement timeline. Understanding when required distributions begin and how they impact your overall tax situation is the foundation of effective RMD planning.

Key Discussion Points

- The RMD rules have changed several times over the past few years, with the required beginning date being delayed from 70 ½ to up to age 75. It’s important to revisit earlier assumptions made for your retirement accounts.

- RMDs generally begin at age 73 for individuals born between 1951 and 1959.

- Individuals born in 1960 or later are expected to begin RMDs at age 75, based on current legislation.

- RMDs apply to most tax-deferred retirement accounts, including traditional IRAs, SEP IRAs, SIMPLE IRAs, and all employer-sponsored retirement plans.

- Roth IRAs (which are not funded with pre-tax contributions) are not subject to RMDs during the account owner’s lifetime.

- The required distribution amount is calculated using IRS life expectancy tables, dividing the account balance by a distribution factor representing the remaining expected lifespan of the recipient.

- Note that inherited IRAs (including Roth IRAs) have their own separate RMD requirements for the beneficiary.

Key Planning Considerations

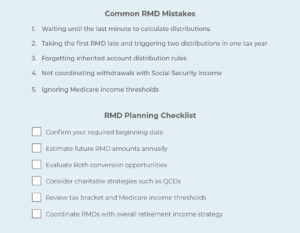

- The first RMD may be delayed until April 1 of the year following the required beginning age. However, delaying the first distribution will result in two taxable distributions in the same year.

- Individuals with multiple IRAs must calculate RMDs separately for each account but may aggregate withdrawals from accounts to achieve the total required distribution. Other types of accounts (including 401(k) and 457(b) accounts) have different requirements for aggregating the withdrawals across accounts.

- Employer-sponsored plans may have different rules, particularly if the individual continues working past the required age.

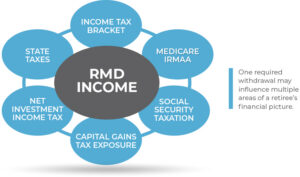

- Distributions from tax-deferred retirement accounts (including RMDs) are taxed as ordinary income in the year of distribution. Large RMDs in retirement may cause increased taxation of social security benefits, the application of IRMAA surcharges, the loss of tax deductions and credits, and a higher tax bracket.

- While RMDs are statutorily defined, you may generally begin taking distributions without penalty at age 59 1/2 and you may always take a larger distribution than the required amount.

Sample Case Study

David, age 73, recently retired after a long career as a senior engineering executive. Over decades of disciplined saving, he accumulated several traditional IRAs and a sizable 401(k) rollover account.

When his first RMD became due, David began withdrawing the minimum amount required each year. However, a closer review of his retirement income picture revealed that his RMD, combined with Social Security benefits and investment income, placed him in a higher tax bracket than anticipated throughout his retirement.

By reviewing his distribution timeline and coordinating withdrawals across accounts earlier in his working career, David would have been able to better manage the tax impact of his RMDs while maintaining a sustainable income stream. In this case David’s deferral strategy ultimately increased his lifetime tax liability.

Key Takeaways

- RMDs represent a mandatory distribution requirement, not necessarily a withdrawal strategy.

- Understanding the mechanics of RMD calculations is the first step in planning.

- The timing of the first RMD may influence overall tax exposure.

The Tax Implications of RMDs

One of the most significant aspects of Required Minimum Distributions is their tax treatment. The vast majority of retirement accounts are funded with pre-tax contributions, making RMD withdrawals taxable as ordinary income.

If you fail to take an RMD in the year it is required you will be subjected to a sizeable penalty of 25% of the amount of the shortfall. In some instances the penalty may be reduced to 10% if you “correct” the failure within two years. Note that the penalty applies in addition to the tax liability arising when the distribution is ultimately made.

For retirees with substantial retirement assets, RMDs can significantly influence your annual tax liability. In some cases, they may also affect other financial considerations such as Medicare premiums, taxation of Social Security benefits, or eligibility for certain tax credits.

The Tax Ribble Effect

Key Discussion Points

- RMD withdrawals are typically taxed as ordinary income.

- Larger RMDs may push retirees into higher marginal tax brackets.

- RMD income may affect Medicare IRMAA surcharges, potentially increasing healthcare premiums.

- RMD income may also influence taxation of Social Security benefits.

- Higher income levels may influence taxation of investment income or capital gains.

Key Planning Considerations

- Strategic withdrawal planning before RMD age may reduce the size of future required distributions.

- Tax diversification across account types may provide greater flexibility in retirement.

- Monitoring income thresholds may help manage potential increases in Medicare premiums.

- Coordinating investment income with required withdrawals may influence overall tax exposure.

Sample Case Study

Karen, a 54-year-old retired physician, accumulated significant retirement assets through decades of saving in tax-deferred accounts. When modeling her financial plan for retirement she realized that once RMDs began, she would be at the highest marginal rate in retirement.

In addition to moving her into a higher tax bracket, the increased income would also trigger higher Medicare premiums due to IRMAA thresholds. Karen began to reduce her pre-tax contributions to her retirement accounts and shifted those contributions into post-tax options. She also worked with her financial advisor to plan for small distributions from her tax-deferred retirement accounts starting in her first retirement year at age 60. Through careful planning and coordination of distributions across her accounts, Karen was able to better manage the tax impact of her withdrawals over time.

Key Takeaways

- RMDs may have broader financial consequences beyond income taxes.

- Understanding income thresholds and tax brackets is an important part of retirement distribution planning.

- Coordination across retirement accounts may help manage taxable income over time.

Strategies for Managing RMDs

Although Required Minimum Distributions are mandatory, individuals still maintain flexibility in how they approach the broader retirement income strategy surrounding those withdrawals. The required amount establishes a minimum, but thoughtful planning may allow retirees to coordinate RMDs with other sources of income, charitable giving strategies, or portfolio management decisions.

Strategy Snapshot – Qualified Charitable Distribution

Key Discussion Points

- RMDs may be used as a source of retirement income.

- Some retirees may reinvest excess distributions in taxable investment accounts.

- Qualified Charitable Distributions (QCDs) may allow certain individuals to direct RMD funds to charitable organizations.

Key Planning Considerations

- QCDs allow individuals age 70½ or older to transfer funds directly from an IRA to a qualified charity. A QCD is not included in the account owner’s taxable income and is not subject to the itemized deduction limitations nor the AGI limits on charitable gifts. By avoiding these limitations the QCD is a much more tax efficient mechanism for making charitable gifts than cash gifts and may be more tax efficient than gifts of appreciated stock as well.

- QCDs are subject to their own annual limitation of $111,000 per person in 2026 and this number is indexed for inflation each year.

- After RMDs begin, QCDs may be used to satisfy some or all of the annual RMD amount.

- By starting QCDs at age 70 ½ the retirement account balance subject to RMDs is reduced without triggering taxes.

- Some retirement accounts (such as a 401(k) account) must be rolled over into an IRA to permit QCDs.

Coordinating RMD withdrawals with other retirement income sources may help stabilize annual income. - Portfolio allocation adjustments may influence which investments are sold to generate distributions.

- Investment decisions surrounding withdrawals may influence long-term portfolio sustainability.

Sample Case Study

Michael and Susan, both in their early seventies, built a substantial retirement portfolio during their careers in law and corporate leadership. While their RMDs exceeded their lifestyle spending needs, they remained actively involved in philanthropic efforts.

By incorporating Qualified Charitable Distributions into their strategy, they were able to direct a portion of their required withdrawals to charitable organizations they supported. This approach allowed them to align their financial planning with their charitable values while managing taxable income.

Key Takeaways

- RMDs can be integrated into broader financial and philanthropic strategies.

- Charitable giving may play a role in distribution planning for some retirees.

- Withdrawal decisions should be coordinated with overall retirement income needs.

Coordinating RMDs with Retirement Income Planning

RMDs rarely exist in isolation. For most retirees, they represent one component of a broader retirement income strategy that may include Social Security benefits, investment income, pensions, and other sources of cash flow.

Coordinating these income streams thoughtfully may help retirees maintain financial stability while preserving long-term investment assets.

Key Discussion Points

- Retirement income may come from multiple sources including pensions, Social Security, and investments.

- RMDs may increase over time as account balances grow or life expectancy factors change.

- Sequence-of-withdrawal decisions may influence portfolio longevity.

Key Planning Considerations

- Aligning RMD timing with other income sources may help stabilize tax exposure.

- Portfolio withdrawals should consider long-term sustainability.

- Monitoring withdrawal rates may help preserve retirement assets.

- Planning decisions made before retirement may influence RMD outcomes.

Sample Case Study

Linda, a former business owner who sold her company in her early sixties, entered retirement with several income streams including investment income, Social Security benefits, and retirement accounts subject to RMD rules.

Because her business sale created a large taxable portfolio, her planning team coordinated RMD withdrawals alongside taxable investment income to help balance annual income levels. This coordinated approach allowed Linda to maintain consistent cash flow while managing overall tax exposure.

Overall Key Takeaways

- Required Minimum Distributions represent an important transition from saving to spending in retirement.

- RMDs may have significant tax implications depending on account balances and income levels.

- Withdrawal strategies should be coordinated with broader retirement income planning.

- Charitable giving strategies may offer opportunities to align distributions with philanthropic goals.

- Thoughtful planning may help retirees manage taxes, preserve assets, and maintain financial flexibility.

Conclusion

Retirement planning often focuses on building assets over time, but the decisions made during the distribution phase may be just as important. Required Minimum Distributions represent a regulatory requirement, but they may also become an opportunity to implement thoughtful withdrawal strategies, manage tax exposure, and align financial resources with long-term goals.

Because each retirement situation is unique, the most effective distribution strategies often depend on a wide range of factors including lifestyle needs, investment portfolios, tax considerations, and family objectives.

Understanding how RMDs interact with other elements of financial planning may help retirees approach the next stage of their financial journey with greater clarity and confidence.

If you would like more information about the terms and strategies discussed in this guide, or if you’re ready to explore how they apply to your specific situation, contact Waverly Advisors. With experience working with individuals, families, and executives managing significant wealth, we specialize in creating tailored strategies with the goal to help you grow, protect, and transfer your assets effectively.